Key Takeaways

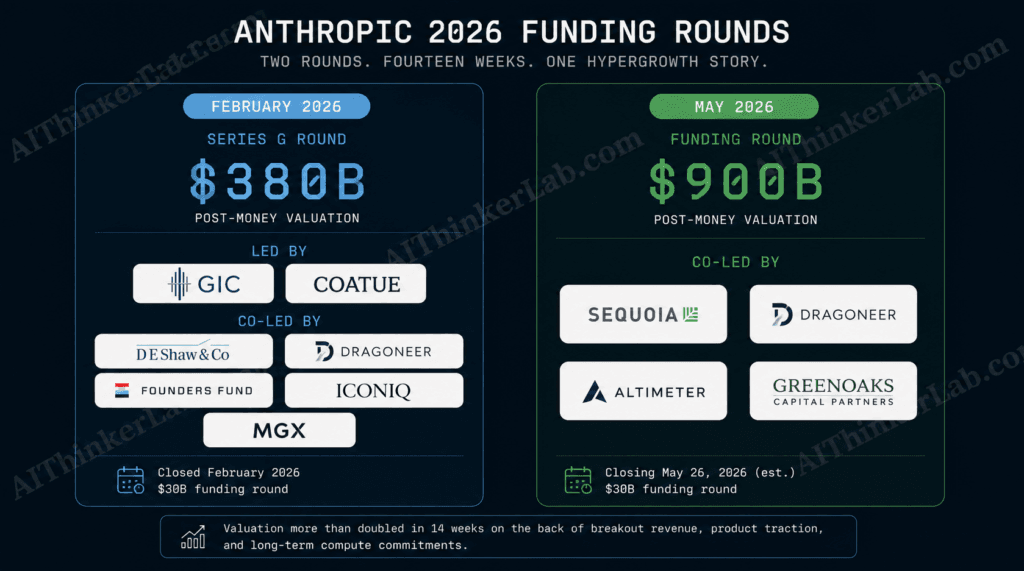

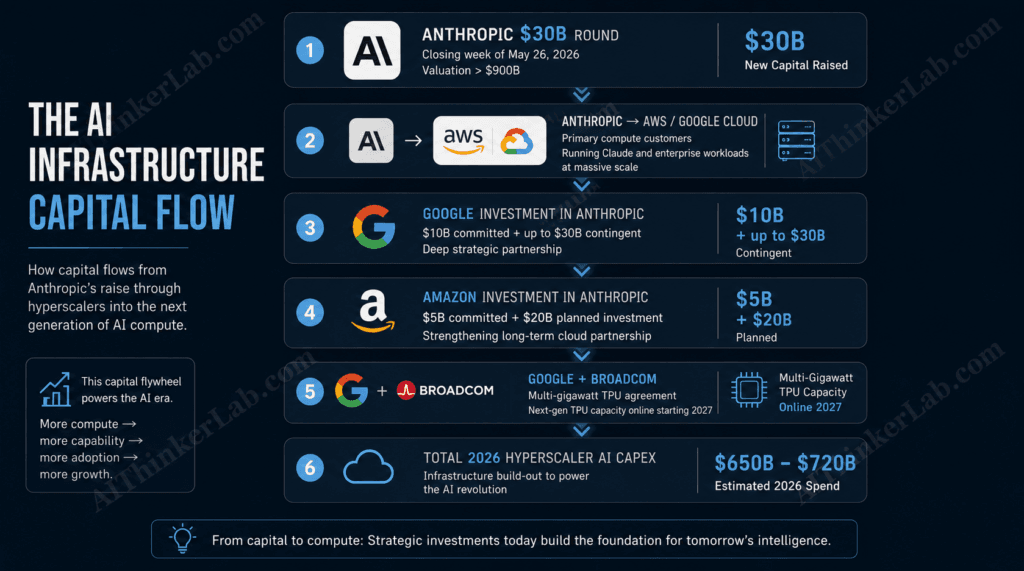

- Anthropic is set to close a funding round exceeding $30 billion at a valuation above $900 billion, as soon as next week (week of May 26, 2026) — moving past OpenAI to become the world’s most valuable private AI company. Bloomberg

- Sequoia Capital, Dragoneer Investment Group, Altimeter Capital, and Greenoaks Capital Partners are each expected to contribute roughly $2 billion as co-leads, doubling Anthropic’s valuation in just 14 weeks from its $380 billion February Series G. Tech Times

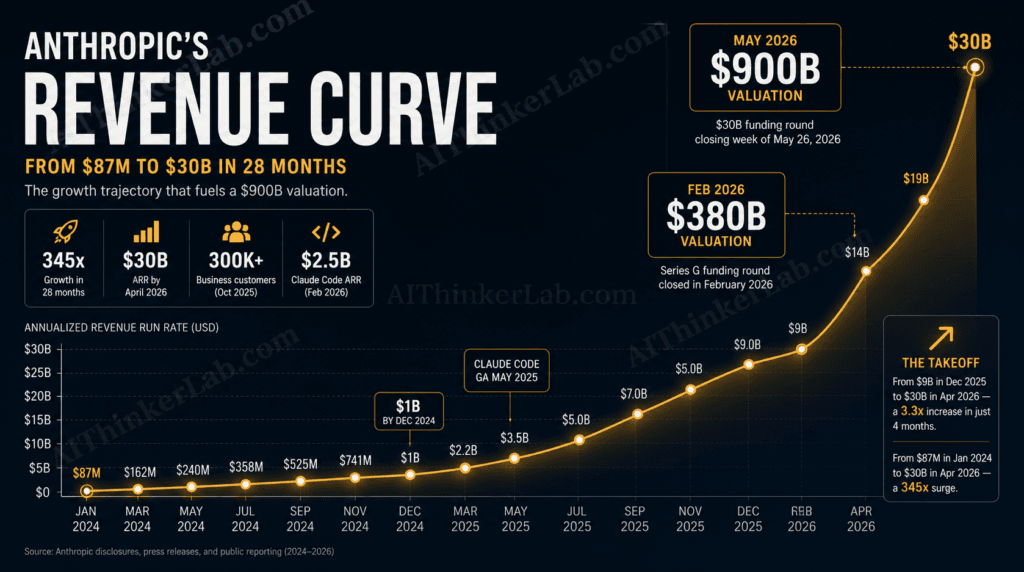

- The number that justified the price: Anthropic’s revenue trajectory — $87 million run rate in January 2024, $1 billion by December 2024, $9 billion by end of 2025, $14 billion in February 2026, $19 billion in March, and $30 billion in April. VentureBeat

- Claude Code became generally available in May 2025, hit $1B in annualized revenue by November 2025, and reached $2.5B in annualized revenue in February 2026, with enterprise use representing over half of Claude Code revenue, customers including Netflix, Spotify, KPMG, L’Oréal, and Salesforce. Sacra

- The capital goes to compute: Anthropic announced a new agreement with Google and Broadcom for multiple gigawatts of next-generation TPU capacity expected online starting in 2027, inside a hyperscaler cycle now running $650–720 billion in 2026 alone. mexc

- The risk the cap table isn’t pricing: Anthropic is also suing the U.S. Department of Defense, which designated the company a supply chain risk in March 2026, with Anthropic estimating the dispute put hundreds of millions to multiple billions of dollars of 2026 revenue at risk. Tech Times

Introduction

The week of May 26, 2026 is closing on what may be the most consequential private financing round in AI history. Anthropic — the maker of Claude — is finalizing a $30 billion raise at a valuation north of $900 billion, the second $30 billion round it’s closed inside a single calendar year. If you’re trying to read what the Anthropic $30B funding round means for the future of AI — where the competitive map is moving, where the cash actually goes, and whether the numbers add up — this piece walks through it with the receipts.

The February 2026 Series G already made the Claude maker the most-funded private AI company outside OpenAI. This May round moves it past OpenAI entirely. The question isn’t whether Anthropic has momentum — the revenue line settles that. The harder question is whether $900 billion is a price that real cash flows will eventually meet, or whether you’re watching the most disciplined growth story of the AI era hit the same gravity that’s been waiting for the rest of the sector.

Inside Anthropic’s $30B Funding Round

The deal closing in late May isn’t Anthropic’s first $30 billion round of the year. It’s the second. Generative AI company Anthropic announced in February that it raised $30 billion in a massive Series G funding round that values it at $380 billion post-money. The financing marks the largest venture funding deal of 2026 so far and the second-largest of all time, per Crunchbase data, following only rival OpenAI’s $40 billion funding in 2025. That earlier round was led by GIC and Coatue, co-led by D. E. Shaw Ventures, Dragoneer, Founders Fund, ICONIQ, and MGX. Crunchbase NewsAnthropic

The May 2026 round is structurally different. Sequoia Capital, Dragoneer Investment Group, Altimeter Capital and Greenoaks Capital Partners are expected to co-lead the financing round, each planning to invest roughly $2 billion. Existing investors including Founders Fund and General Catalyst are also expected to participate. Anthropic leadership began considering the $900 billion price tag after receiving several unsolicited proposals from interested investors in recent weeks. BloombergYahoo Finance

Why two raises in 14 weeks? Revenue ran ahead of every internal forecast. And the capital push comes as the San Francisco-based company explores a potential initial public offering as early as October. Stacking capital before a public listing isn’t unusual; doing it while more than doubling your valuation in a single quarter is. If you’re tracking the broader picture, our breakdown of the 2026 AI IPO calendar sets the context for what’s coming. Yahoo Finance

The Revenue Curve That Justified $900 Billion

Here’s the number that makes the rest of the story make sense. Anthropic’s annualized revenue run rate surged from $87 million in January 2024 to $30 billion by April 2026 — a pace that CEO Dario Amodei said outstripped the company’s own forecasts by a factor of eight. VentureBeat

Read the curve again: $9 billion to $30 billion in roughly four months. For context: Salesforce took about 20 years to reach $30 billion in annual revenue. Anthropic did it in under three years from a standing start. VentureBeat

Two engines are running underneath. The first is Claude Code, Anthropic’s agentic coding tool — covered in detail in our Claude Code for enterprise developers guide. Claude Code, launched publicly in mid-2025, reached $1 billion in annualized revenue within six months. The Model Context Protocol (MCP), Anthropic’s open standard for connecting AI agents to external tools, crossed 97 million installs in March 2026. The second engine is API consumption through cloud resellers: As of October 2025, Anthropic had 300,000+ business customers accounting for approximately 80% of revenue, with 100,000+ of those running Claude on Amazon Bedrock as of April 2026. MediumSacra

The pricing isn’t fluff. Number of business customers spending over $1 million annually doubled to more than 1,000 in under two months following the February Series G. Two years ago, only a dozen customers exceeded $1 million annualized spend. MLQMLQ

The “so what” for you: When a model vendor doubles its $1M+ accounts in eight weeks, the spend is no longer experimental. Procurement has signed off. Workflows are dependent. That’s the kind of revenue venture investors will pay 30x for — and it’s the kind public markets traditionally won’t argue with.

Why Sequoia, Dragoneer, Altimeter, and Greenoaks All Said Yes

Three of these four firms — Sequoia, Dragoneer, and Altimeter — were already on Anthropic’s cap table from earlier rounds. None is writing a $2 billion check on momentum alone.

OpenAI’s $852 billion valuation is facing skepticism from some of its own investors as the company scrambles to reorient itself around enterprise customers and fend off Anthropic, according to the Financial Times. One investor who has backed both companies told the FT that justifying OpenAI’s round required assuming an IPO valuation of $1.2 trillion or more — making Anthropic’s current $380 billion valuation look like the relative bargain. The secondary market tells a similar story right now, where demand for Anthropic shares has grown nearly insatiable while OpenAI shares are trading at a discount. TechCrunchTechCrunch

There’s also a margin story. Anthropic’s training costs are projected at roughly a quarter of OpenAI’s over the same period, and the company expects to reach profitability by 2028 or 2029, years ahead of its rival. For a pre-IPO investor, that distinction matters more than a few hundred billion in valuation: it’s the difference between buying a growth story and buying a leverage story. Proactiveinvestors NA

According to CNBC, approximately 80% of Anthropic’s business comes from enterprise customers — a significantly higher enterprise mix than OpenAI, which generates more consumer revenue through ChatGPT subscriptions. Enterprise revenue is stickier, renews more reliably, and supports the multiples a public market will eventually be asked to honor. If you want the strategic context, our Claude vs ChatGPT for the enterprise comparison goes deeper into the buyer-side calculus. AI Business Weekly

How the Anthropic $30B Funding Round Reshapes the Competitive Map

Before the May raise, the AI frontier looked like a two-horse race with OpenAI ahead by valuation and Anthropic ahead by growth rate. After it, the order flips on both measures.

The downstream effects are showing up in public markets too. The competitive dislocation is already visible: Anthropic’s Claude Cowork and Claude Code products have triggered a broad repricing of enterprise software, with Salesforce and ServiceNow each losing approximately a third of their market value. That’s not a forecast — it’s a repricing already in motion. IG

| Metric | Anthropic (May 2026) | OpenAI (Latest) |

|---|---|---|

| Latest valuation | ~$930B post-money (closing) | $852B (March 2026) |

| Annualized revenue run rate | $30B (April 2026) | ~$25B (early 2026) |

| Revenue growth (15 months) | ~30x | ~25% |

| Enterprise revenue share | ~80% | Smaller; ChatGPT-led |

| Flagship growth product | Claude Code ($2.5B ARR) | ChatGPT (~900M WAU) |

| 2026 projected loss | Path to profitability by 2028–29 | $14B projected loss |

| IPO target | October 2026 | 2026, confidential filing |

Sources: Bloomberg, VentureBeat, Sacra, Proactive Investors, IG (Feb–May 2026)

The number that matters most in that table isn’t valuation. It’s the loss line. A company guiding to profitability inside three years gives public investors a price they can stress-test against future free cash flow. A company projecting a $14 billion loss for 2026 against roughly $18 billion in revenue is asking for a continued act of faith. Proactiveinvestors NA

Where $30 Billion Actually Goes: The Compute Question

Anthropic doesn’t need cash for marketing. It needs cash for compute, and the timing of this raise reveals which compute.

Anthropic announced a new agreement with Google and Broadcom for multiple gigawatts of next-generation TPU capacity expected online starting in 2027. The company published a statement noting the deal represents its most substantial compute commitment to date. That deal sits on top of staggering big-tech commitments: Google committed to invest $10 billion in Anthropic at a $350 billion valuation, the same amount it was valued at in a $30 billion funding round in February. The Alphabet Inc.-owned company plans to invest up to another $30 billion in Anthropic if the startup hits certain performance targets. Amazon.com Inc. is also investing $5 billion in Anthropic at a $350 billion valuation, with plans to inject $20 billion more over time. mexcYahoo Finance

Anthropic is being financed not just by traditional venture firms but by the same hyperscalers it depends on for compute. Amazon, Alphabet, Microsoft and Meta, the four largest cloud and technology platforms, accounted for $650 to $700 billion in capital expenditures (capex) for 2026. That is nearly double what the same group spent in 2025, and larger than the GDP of most countries. Goldman Sachs’ baseline model implies $765 billion in annual AI CapEx in 2026, growing to $1.6 trillion in annual CapEx in 2031. Ferguson WellmanGoldman Sachs

In that context, Anthropic’s $30 billion is roughly a single year’s compute budget for an upper-tier frontier lab. For the broader infrastructure picture, our 2026 AI capex trends breakdown maps the full hyperscaler spending cycle.

The Contrarian Case: When Even Sequoia Might Be Wrong

You don’t need to be a permabear to take the bubble warnings seriously, and the most credible ones aren’t coming from short sellers.

The Monetary Authority of Singapore warned that some Big Tech firms, primarily hyperscalers, have turned to the use of novel and potentially circular private financing arrangements to fund their expansions, including the use of special purpose vehicles, private credit structures and novel accounting treatment that could mask leverage and increase funding dependencies. Anthropic sits squarely inside that loop. Consider the web at the center of the AI economy: Nvidia invested in OpenAI stock, then committed $100 billion to OpenAI — money that will be largely spent purchasing Nvidia’s own products. Microsoft owns approximately 27% of OpenAI and is OpenAI’s primary cloud provider through Azure, generating Azure revenue that gets reinvested in Nvidia chips. Amazon is a major investor in Anthropic, which committed to using Amazon Web Services as its primary cloud provider. mexcMedium

The second crack is what CNBC called the “cheap AI” problem. At nearly trillion-dollar valuations each, the S-1 has to show enterprise revenue growth and concentration that justifies the multiple. But the premium that justifies the valuation is eroding fastest in exactly the segments the labs need to dominate. And the cheap alternatives are no longer a step behind. If the premium on a frontier-class model collapses, so does the spread that pays for $200 billion data centers. We dig further into this dynamic in our open-source vs frontier AI economics piece. CNBC

The third risk is regulatory. Anthropic faces regulatory scrutiny in the United States. The company is contesting a federal designation that labeled it a potential supply chain risk, a move it has warned could cost billions in lost revenue. The dispute has introduced uncertainty among some enterprise customers, with more than 100 reportedly raising concerns about continuing their relationships with Anthropic, according to Bloomberg. PYMNTS

The contrarian read isn’t that Anthropic is overvalued in absolute terms. It’s that the price assumes nothing breaks. At $900 billion, almost everything has to keep working: enterprise demand keeps compounding, the DoD case resolves cleanly, open-model competition stays subscale, and compute deliveries arrive on schedule. That’s a lot of dependencies riding on one number.

What This Means for Enterprise AI Buyers Right Now

If you’re inside an enterprise evaluating AI infrastructure, the Anthropic $30B funding round shifts your decision in three concrete ways.

First, vendor durability is no longer the question it was 18 months ago. A company with $930 billion of market cap, $30 billion of annualized revenue, and 1,000+ million-dollar enterprise accounts is not a vendor your procurement team can dismiss on stability grounds. The risk has flipped: the question isn’t whether Anthropic will exist in five years; it’s whether you’ll be late to standardize on it. Our enterprise AI procurement playbook walks through how to handle that conversation with finance.

Second, pricing power is moving toward Anthropic, not away. Eight of the Fortune 10 companies are currently running critical workloads on Claude. That level of penetration among the world’s most powerful corporations reflects growing institutional trust in the platform. When 80% of the top of the Fortune 10 has standardized, the negotiating leverage of any individual buyer drops. Model switching costs are real. Map them now, before they become structural. mexc

Third, the compute pipeline now favors Anthropic for the next 12–18 months. With the Google–Broadcom TPU deal coming online in 2027, Anthropic’s inference and training capacity will expand faster than the broader market’s. If you depend on rate limits, latency guarantees, or long-context throughput, that’s a tactical advantage that your competitors will also have access to. The “so what” for you: don’t read this round as a vanity number. Read it as a signal about which AI stack will have the throughput, customer references, and survival odds to be your standard infrastructure by 2028.

What Anthropic’s $30B Funding Round Means for the Future of AI

Three structural shifts follow from this round, regardless of whether the bubble warnings turn out to be right.

Frontier AI is now a two-firm oligopoly with a Chinese asterisk. Between them, Anthropic and OpenAI have raised roughly $200 billion in private financing. Every other Western foundation-model lab has raised an order of magnitude less. The capital intensity of frontier training has effectively closed the door behind them — outside China, where DeepSeek, Qwen, and others are competing on a different cost curve entirely.

The Anthropic–Amazon–Google triangle is now AI’s most consequential commercial relationship. Anthropic depends on both AWS and Google Cloud for compute. Amazon and Google together have committed to over $80 billion in potential investment. Whatever Anthropic does — pricing, model release cadence, safety posture — ripples through two of the three largest cloud businesses on earth. That’s a level of vendor concentration that would have triggered antitrust scrutiny in any other industry a decade ago. Our analysis of AI vendor concentration risk walks through what that means for buyers.

The IPO window matters more than the funding round. A successful October 2026 listing at or above $900 billion would set the first public-market benchmark for pure-play frontier AI. If it holds, it validates the entire private-market valuation stack. There are now 498 AI unicorns (companies valued at over $1 billion) globally. If the listing breaks, it triggers a repricing of every one of them behind it. Medium

The Reading on May 23, 2026

Treat the Anthropic $30B funding round as two data points, not one. The February Series G told you the company had crossed from “frontier lab” to “enterprise platform.” The May round, closing this week at $900 billion-plus, tells you the market has decided it’s the winner of that platform fight — at least until the IPO has to defend the number in front of public investors.

That’s a real verdict, not a hype cycle. Anthropic’s $30 billion run rate, 1,000+ million-dollar accounts, and 80% enterprise mix are not numbers you fabricate in a deck. The skeptics don’t really dispute them. What they dispute is whether $900 billion correctly prices the dependencies — the Pentagon case, the circular financing, the open-model creep, and the assumption that compute capacity scales linearly into 2027.

If you’re a buyer, your move is to assume Anthropic is durable and negotiate against that durability now, while there’s still slack in the system. If you’re an investor, your move is to watch the October IPO; that’s where the conviction gets tested with real liquidity. And if you’re a builder, the more useful reading is upstream: this round is the clearest signal yet that the AI economy is consolidating around two firms, on two clouds, with one IPO calendar to defend. The next 12 months will decide whether that’s a stable equilibrium or the moment a single failure resets the whole stack.

References

- Anthropic — Series G Funding Announcement — primary, February 12, 2026

- Bloomberg — Anthropic to Close Over $30 Billion Round — primary news, May 22, 2026

- Bloomberg — Anthropic in Talks to Raise $30 Billion at $900 Billion Valuation — May 12, 2026

- VentureBeat — Anthropic Hits $30B Revenue Run Rate After 80x Growth — May 2026

- Sacra — Anthropic Revenue, Valuation & Funding Tracker — May 2026

- TechCrunch — Anthropic’s Rise Gives OpenAI Investors Second Thoughts — April 15, 2026

- Crunchbase News — Anthropic Raises $30B at $380B Valuation — February 12, 2026

- Goldman Sachs — Tracking Trillions: AI Build-Out CapEx — March 2026

- CNBC — Cheap AI Could Derail OpenAI and Anthropic’s IPOs — May 20, 2026

- Proactive Investors — Wall Street Braces for a Trillion-Dollar AI Stampede — May 2026

- PYMNTS — Anthropic Hits $30B Run Rate as Enterprise Demand Accelerates — April 2026

- TechTimes — Anthropic Funding Round to Top $30B — May 23, 2026